🏋️ Aditya Khemka's Winning Framework:

“Inside the Mind of a Healthcare Stock Picker: How Aditya Khemka Builds Alpha Using Cash Flows, Pricing Power & Small-Cap Discipline”

🔹 What You Can Expect From This Post

In this post, you’ll uncover:

🥇 The 5-point financial evaluation framework Aditya Khemka uses to select stocks

🚀 His sectoral playbook within pharma and healthcare

📊 The key differences between secular compounders and cyclical pharma bets

❌ What he avoids (like US generics) and why

If you’re starting your investing journey or want to understand how India’s top healthcare-focused fund manager thinks, this will be your mental model cheat sheet.

💼 Meet Aditya Khemka

Aditya Khemka manages a ₹550 Cr healthcare-focused portfolio at InCred AMC. His investment style is:

Highly concentrated (12-13 stocks)

Skewed toward small caps (80% of portfolio)

Deeply focused on branded, essential, cash-generating businesses

Before InCred, he worked with DSP BlackRock, Nomura, Ambit, and Antique. His track record in the healthcare sector is both long and stellar.

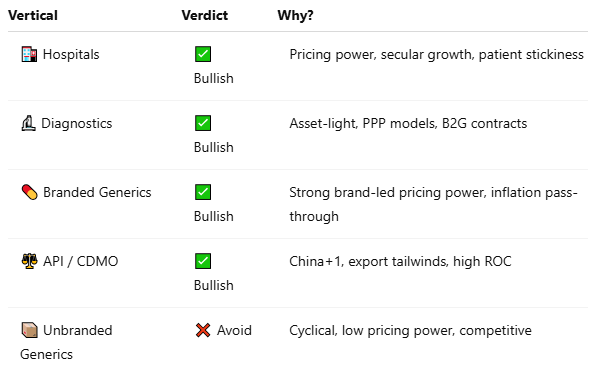

🦇 Sectoral Playbook: Not All Pharma is Equal

Khemka doesn’t bucket pharma into one group. Instead, he breaks it down into 5 verticals:

His preference is companies with recurring demand, niche dominance, and high margins.

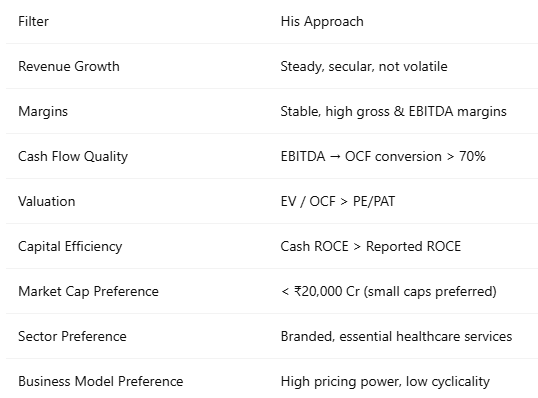

🧰 The 5-Point Financial Framework

📈 1. Secular Topline Growth

Prefers non-lumpy revenue compounding (e.g., 8-12% annually)

Avoids businesses with wild topline swings

🧵 2. Margin Stability

Both gross and EBITDA margins must be stable

Reflects durable pricing power

💸 3. High Cash Conversion

Focuses on EBITDA to Operating Cash Flow conversion

80%+ conversion is ideal; 10-20% is a red flag

🤝 4. EV / Operating Cash Flow (Valuation)

Uses this over P/E or EV/EBITDA

Captures working capital & debt impact, giving truer picture

📉 5. Cash ROCE (Cash Return on Cash Invested)

Emphasis on cash returns, not accounting profits

High CROCI = high quality business

🔒 What He Avoids

🤔 US Generic Exporters

Tariff risks, wafer-thin margins, high competition

E.g. Lupin, Aurobindo, Cadila

🚫 Unbranded Generic Companies

No brand loyalty = no pricing power

Highly volatile earnings

💰 Bottom Line: The Khemka Filter

📊 Your Investing Takeaway

Don’t bucket all pharma stocks the same. Look deeper into business model, margin quality, and cash generation.

Aditya Khemka’s framework is a masterclass in business quality evaluation, especially for healthcare.

Use this post as your reference guide to:

Avoid false positives in pharma

Focus on cash-rich secular compounders

Build conviction the way seasoned fund managers do

Source:

PS: Exact Transcript of - Aditya Khemka’s 5-Point Business Evaluation Framework

“So the financial parameters we look at—there are four or five parameters, I’ll take you through them one by one.

📈 1. Secular Topline Growth

How consistently has the company been able to grow over the past decade. Right? So if you notice the topline growth of unbranded generic companies, some year they will do 40% topline growth. The next year they will be down 30%—because, you know, in a given year they launched a differentiated product and then it later got competitive. So they lost all their market share in pricing.

That happens in unbranded players.

In a branded player what you will see is—they will grow every year. Some years they will grow 5%, some years they will grow 12%, some years they will grow 15%. But in no year they will grow 40%, and in no year they will have a decline in revenue.

So the secularity of earning growth—the topline growth—is very important to us.

🧵 2. Margin Stability

Maintenance of margins, both gross and EBITDA margins. So if you have pricing power, that should reflect in the fact that your gross margin will be very less volatile. Your EBITDA margin also will be very less volatile.

💸 3. High Cash Conversion

Your ability to convert the profit to cash, so the EBITDA to operating cash flow conversion—that is very important to us.

So if you’re earning ₹200 crores of EBITDA but your cash flow is going to be ₹20 crores, that EBITDA is of no good use to me.

Whereas if you’re generating ₹100 crores of EBITDA and out of that ₹100 crores ₹80 crores is getting translated to operating cash flow—that’s an asset I want to own.

\n>

🤝 4. EV / Operating Cash Flow (Valuation)

So in terms of valuations, we definitely look at EV to operating cash flow as a metric.

Now, why EV to operating cash flow?

One—EV takes account of debt or net cash, whatever you might have on your balance sheet, other than just the market cap.

And why operating cash flow? Because operating cash flow includes the impact of working capital on your profitability, which is left out when you look at EBITDA or PAT as a valuation number.

So that is why we look at EV to operating cash flow.

📉 5. Cash ROCE (Cash Return on Cash Invested)

We look at is cash return on cash invested, which is the equivalent of cash ROCE.

So we look at return on capital employed, but we look at cash return on capital employed.

So there are multiple companies today that might have ₹200 crores of PAT but only ₹20 crores of operating cash flow.

But there are companies also which have ₹50 crores of PAT and ₹100 crores of operating cash flow.

So as the asset manager I’m only concerned about the cash that the company generates—I’m not concerned about what profit it’s reporting.

So I will look at cash return on cash invested, which is CROCI.”*